How to choose the ideal group savings accounts for your employees

Want to attract and retain top talent? Offering the right mix of group savings accounts can make all the difference. Read on to learn how to build a plan your employees will love.

March 17, 2025

What keeps your employees up at night? For some, it’s saving for a down payment on a house. For others, it’s their retirement portfolio. For the true insomniacs, it could be both.You can help your employees reclaim their beauty sleep — and it just so happens that playing the hero helps you too. Our research found that over 90% of people are more committed to companies offering great benefits — including a stellar group savings plan.

What are group savings plans, anyway?

Group savings plans are a simple way for companies to help their workers prepare for the future by setting up automatic deductions from pay cheques that go into special investment accounts. Many employers offer contribution matching programs as an added benefit of employment.

There are different types of accounts you can offer, which serve distinct purposes. Some are laser-focused on retirement savings, while others offer more flexibility for things like buying a first home or building an emergency fund. The magic happens when you combine them in ways that support your employees’ many financial goals.

HR considerations

Choosing the right mix of savings plans isn’t a decision you want to make without proper planning. First, let’s look at the key factors that should shape your strategy.

Employee demographics

To pick the right plan, you can look at:

- Age distribution across your organization

- Dispersion of income levels

- Life stages and financial priorities

- Geographic location and cost-of-living realities

Company budget

Assess your financial resources:

- What level of matching contributions can you sustainably offer?

- How might your budget evolve as your company grows?

- What’s the right balance between retirement and other savings incentives?

It’s better to start conservative and scale up than to overpromise and have to claw back.

Administrative complexity

You need to make sure your plan works for you. Take inventory of the following things:

- Current payroll and HR team capacity

- Your HR tech stack and available integrations

- Employee education and support resources

- Reporting and compliance requirements

When working with a partner (like us!), you should determine how well they can match your needs. Can they plug into your current HR systems? How much educational material do they provide? What do management fees look like?

Tax implications

Not even your accounting team likes talking about taxes, but they need to be in the conversation for both your organization and your employees.

For your organization:

- Tax treatment of employer contributions

- Payroll tax considerations

- Compliance and reporting obligations

For your employees:

- Tax advantages at different income levels

- Immediate versus deferred tax benefits

- Impact on government benefits

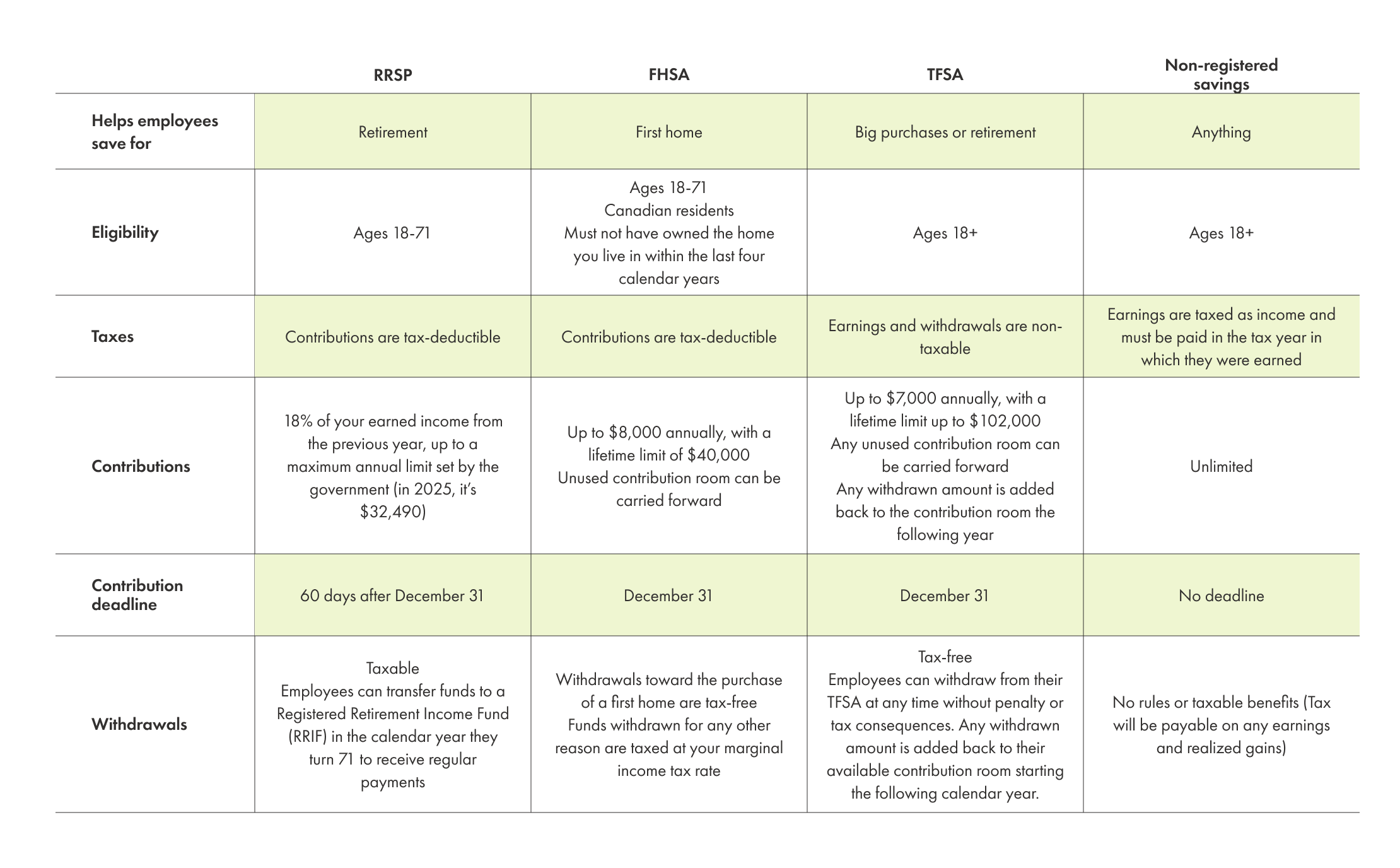

Types of accounts to offer

To avoid overcomplicating things, we’re going to focus on the four most common types of group savings accounts. If competition for talent is really stiff, there are even more options you may want to consider, including the Deferred Profit Sharing Plan (DPSP).

Group RRSP

The foundation of many corporate savings programs, Group RRSPs offer tax-deferred retirement savings with the convenience of automatic payroll deductions.

Key benefits for you:

- Powerful tool for attracting and retaining talent

- Tax-deductible matching contributions

- Simpler to administer than traditional pension plans

- Helps employees build long-term financial security

Employee advantages:

- Immediate tax relief through payroll deductions

- Potential employer matching

- Lower management fees than Individual RRSPs (in most cases)

- Tax-deferred investment growth

Implementation considerations:

- Decide on matching contribution levels (we see average matching between 4% and 5%)

- Choose between restricted and unrestricted withdrawal options

- Plan for regular employee education and engagement

- Consider vesting periods for employer contributions

Group FHSA

Introduced in 2023, an FHSA combines RRSP-like tax deductions with TFSA-style tax-free withdrawals for first-time home purchases, with set annual and lifetime contribution limits.

Key benefits for you:

- Attracts younger employees focused on homeownership

- Demonstrates support for major life goals

- Complements existing retirement savings options

- Positions your organization as forward-thinking

Employee advantages:

- Tax-deductible contributions of up to $8,000 annually

- Tax-free withdrawals for first home purchases

- Flexibility to transfer unused funds to an RRSP

- Combined benefits of RRSP and TFSA features

Implementation considerations:

- Best offered alongside other savings options

- Clear communication about eligibility requirements

- Education about the 15-year time limit

- Strategy for employees who already own homes

Group TFSA

Group TFSAs are a great option for short- or long-term savings goals, with unused contribution room being carried forward each year. They offer the advantages of accessible, tax-free savings for major life expenses, emergencies, or supplemental retirement income.

Key benefits for you:

- Appeals to employees across all income levels

- Complements retirement-focused options

- Simple administration and setup

- Supports diverse financial wellness goals

Employee advantages:

- Tax-free investment growth and withdrawals

- Flexible access to funds when needed

- No impact on government benefits

- Contribution room restored after withdrawals

Implementation considerations:

- Determine whether to offer employer contributions

- Plan for educational support about optimal usage

- Consider integration with other savings options

- Develop a strategy for encouraging consistent contributions

Group Non-Registered Savings Account

A Group Non-Registered Savings Account provides additional savings capacity beyond registered plans, with no contribution limits but no special tax treatment.

Key benefits for you:

- Simple administration

- Attractive to high-income employees

- Complements tax-advantaged options

Employee advantages:

- Unlimited contribution potential

- Complete flexibility for withdrawals

- Access to the same investment options

- No age restrictions

Implementation considerations:

- Usually best as a supplemental option

- Clear communication about tax implications

- Integration with other group plans

- Focus on high-income employee needs

How to build an optimal plan for your team

Now that you understand the different group savings options, it’s time to build your plan.

Based on our experience designing financial benefits programs for thousands of companies, here’s how to build one effectively:

1. Know what your organization needs

Before implementing any plans, lean on real data.

- Survey your team to understand their financial goals and preferences.

- Research what similar organizations in your industry and region offer.

- Determine what you can reasonably afford, both now and in the future.

You can also get in touch with one of our team members for support.

2. Design your plan structure

Most successful companies start with a Group RRSP (with employer matching) as their foundation, then add complementary options like TFSAs or FHSAs.

If this seems like too much to do all at once, consider a staged rollout of your full program. For example:

- Year 1: Group RRSP with 3% matching

- Year 2: add Group TFSA option

- Year 3: introduce FHSA and potentially increase RRSP matching

Determine how much you can afford to offer employees, and which option you want to utilize.

Wondering what contribution level to set? Wealthsimple for Business employers we work with, that offer matching, are offering between 4% and 5% on average, with the median being 4%.

3. Create a communication strategy

To make your plan effective, you have to prioritize education. Ensure new and old employees alike know about, and enrol in, your plan. Make it a touchpoint within onboarding, and regularly reach out to employees who aren’t enrolled.

If you notice certain employees keep saying they’re going to enroll but don’t, focus on education. Even simple guidelines can empower employees, driving enrollment by helping them choose the right account.

For example, you could share the following sort of content or direction for employees based on their savings goals:

- No specific savings goals: go with the account with employer matching

- Aspiring homebuyers: prioritize FHSA

- Building emergency funds: focus on TFSA

- Within peak earning years: maximize RRSP contributions

4. Optimize administration

Time can often be the biggest barrier to creating good financial benefits programs. More specifically, administrators’ time. You can circumvent this by:

- Choosing providers with integrated platform solutions (and a guide on how to use it)

- Streamlining enrollment and contribution processes

- Leveraging technology for employee self-service

- Set up automatic monitoring for participation and satisfaction metrics

Implementing your plan

With your plan selected, implementation requires understanding who handles what. Here’s how responsibilities should typically be shared between your team and the plan provider:

What you handle

- Assign dedicated HR resources to manage the program

- Set up enrollment, contribution, and reporting processes

- Plan your employee communication strategy

- Build knowledge of key regulatory requirements

Your partner’s contribution

- Provide expertise in plan design and compliance

- Deliver ready-made educational materials

- Offer administrative technology to simplify management

- Share insights from similar organizations’ experiences

Wealthsimple can help

Our team specializes in designing and implementing customized savings plans for a range of organizations. Contact us and we can help you create an effective program your employees will love.